If you're behind on a couple of bills, juggling Afterpay payments, and the supermarket shop stings a bit more than it used to, you're not the only one, and you haven't done anything wrong.

The cost of living has gone up everywhere. Fuel prices spiked 32.8% in March 2026 alone, the largest single-month jump since ABS records began in 2017. Housing was up 6.5%. Groceries keep climbing, and the average household is now spending around $207 a week on food (closer to $240 if you've got a family of four). Wages haven't kept up. People who managed fine a couple of years ago are suddenly finding themselves short at the end of every pay cycle.

If you're in that spot, owing a few thousand on a credit card, an Afterpay balance, maybe a personal loan, or an unpaid power bill, the good news is that debt at this level is usually something you can sort out yourself. You just need a plan.

Here's one that works for the way Australians actually live in 2026: Afterpay, food delivery, four streaming subscriptions and all. There's also a free budget planner spreadsheet you can download near the end.

You can't fix what you can't see. Most people in financial stress can tell you how much they earn, but only a rough guess at what goes out. The difference is bigger than expected.

Get a piece of paper, a spreadsheet, or open the notes app on your phone. Set the time period to match your pay cycle, weekly, fortnightly, or monthly. Then list every single thing that leaves your account.

A modern Australian budget needs to capture a lot more than it did a decade ago. Here are the categories most people miss:

Income

Household

Transport

Food

Personal and family

Debts

Savings

Once it's all on the page, add up your income and subtract your expenses. The number you get is the truth. If it's positive, you have something to work with. If it's negative, you're not bad with money; you're insolvent on paper, and you'll need to either cut harder, earn more, or look at the help options later in this article.

The old version of this advice would tell you to skip your $4.50 coffee. That's not where the money goes anymore. In 2026, the silent budget killers look different.

Afterpay, Zip, Klarna, and Humm are designed to make you feel free. They actually aren't. A $200 jacket on Afterpay is still $200, and once you've got four or five plans running across two or three apps, the fortnightly auto-debits stack up to a chunk of your pay you never actually decided to spend.

Research by Finder suggests roughly 41% of Australians have used BNPL recently, and around 57% of younger Australians use it. One in three young BNPL users has missed another bill to make a BNPL repayment, and 12% have skipped a meal.

If that's you, you're not failing. You're using a product designed to make spending feel painless. The fix is to look at it on one page: log into each app, write down every active plan, and add up the next two months of payments. That number is what your "free" purchases actually cost.

Most households are now running 5-10 active subscriptions without realising it. Streaming alone can easily top $90 a month. Add Spotify, a gym, a couple of apps you forgot you signed up to, ChatGPT, an Adobe plan, cloud storage, and you're at $150–$250 a month for things you barely use.

Open your bank statement for the last three months and circle every recurring charge. Cancel anything you wouldn't actively re-buy today.

Uber Eats and DoorDash are convenience services that quietly cost 2 to 3 times what cooking the same meal costs. If you're ordering even twice a week at $35 a pop, that's roughly $3,600 a year.

Capping yourself to once a fortnight, and using grocery click-and-collect for the in-between, can free up $200+ a month with very little lifestyle impact.

Cash makes spending feel real. Tapping your card or watch doesn't. If you're losing track of where the money goes day-to-day, try a one-week cash test for one category, usually takeaway or coffee. Withdraw the budget in cash on Monday. When it's gone, it's gone.

Most people are shocked at how quickly $100 disappears when they have to physically hand it over.

This one's older but still true. There's no point switching to home-brand pasta to save 50 cents a week if you've just signed up for a $2,500 lounge suite on a 24-month interest-free deal.

The big-ticket commitments matter far more than the small daily ones. Before you sign anything that locks you into ongoing payments, ask: Can I genuinely afford this if my hours get cut for a month?

Paying down debt while taking on new debt is like bailing out a boat with the tap still running. You'll exhaust yourself for nothing.

Before you make a single extra repayment, do this:

None of this is about willpower. It's about making it harder to spend without thinking. Just like it's easier to eat well when there's no junk food in the house, it's easier to stop spending when the spending tools aren't within easy reach.

This sounds counterintuitive when you owe money, but it's the most important step of all. Without a small buffer, even $1,000 to $2,000, the first surprise expense (car battery, fridge, school excursion, vet bill) will put you straight back onto the credit card or BNPL.

Pick a number you can realistically hit in 4 to 8 weeks. $1,500 is a sensible 2026 target, enough to cover most minor emergencies, not so high that it feels impossible. Put it in a separate savings account, ideally at a different bank from your everyday account, and don't link it to your debit card.

Then leave it alone. This money exists for one job only: to stop a small problem from turning into a new debt.

With the emergency buffer in place and new debt paused, now you focus on clearing what you owe.

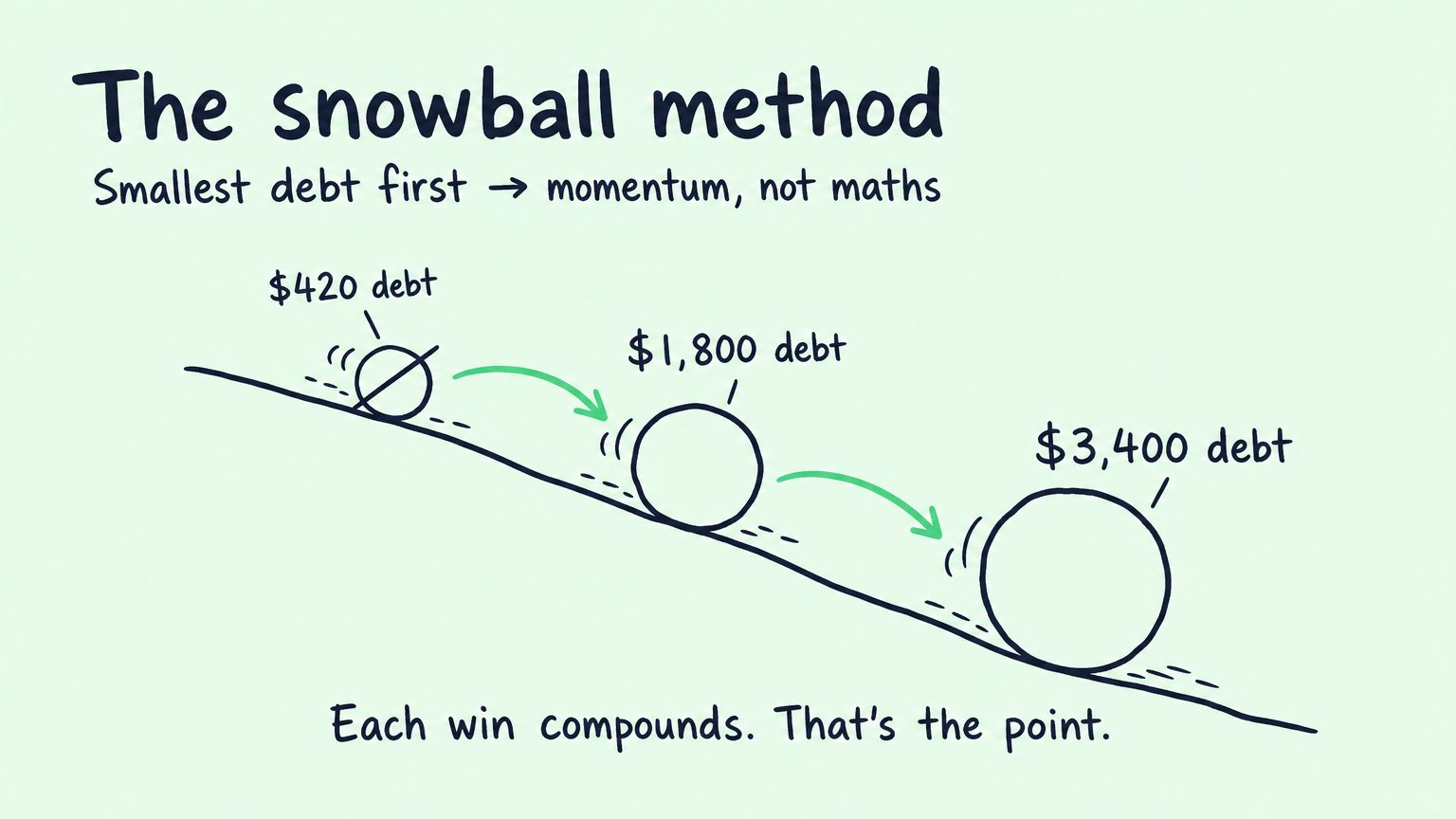

List every debt you have. Include the balance, the minimum repayment, and the interest rate or late fee. Then sort them by balance, smallest at the top, largest at the bottom.

Pay the minimum on everything except the smallest debt. On that one, throw every extra dollar you've got. When it's gone, take the money you were paying on debt one (extra + minimum) and roll it into debt two. Then debt three. And so on. The "snowball" grows as you go.

Mathematically, paying the highest interest rate first saves you slightly more money. But in the real world, the snowball method works better for most people, because each cleared debt feels like a win, and wins are what keep you going when things are hard. Most people who get out of debt do it on motivation, not maths.

A common alternative pitched online is a debt consolidation loan or a balance transfer credit card. Be careful with these. ASIC's research has found that about 30% of people who balance-transferred ended up with more debt than they started with, because they kept using the original card alongside the new one.

If you go down that path, only do it if you have rock-solid discipline to close the old account the day the transfer clears.

Most Australians don't know they can now legally ask Afterpay to pause their payments.

If you can't make a repayment on a regulated credit product in Australia, you have the legal right to request a financial hardship variation. That means asking your creditor to temporarily reduce your payments, pause them, or restructure the loan term.

This has been the law for years under the National Consumer Credit Code for credit cards, personal loans and car loans.

From 10 June 2025, those same rules apply to BNPL providers. Afterpay, Zip, Klarna, Humm and the rest are now regulated as "low-cost credit contracts" under the National Consumer Credit Protection Act 2009.

They must hold an Australian Credit Licence, they must be members of the Australian Financial Complaints Authority (AFCA), and they must respond to a financial hardship request within 21 days.

What that means in practice: if you're struggling to make an Afterpay or Zip payment, you don't have to ghost the app and accumulate late fees. You can ask for a hardship variation, in writing, the same way you would with a bank.

You’re not asking for a favor, this a legal right. Creditors expect these calls. It's part of how the system works. They generally prefer working with you than chasing a default.

If any part of this feels overwhelming, and it's normal if it does, you don't have to do it alone. There are free, government-funded services that exist exactly for this situation.

None of these services costs a cent. None of them will judge you. All of them deal with people in your situation every single day.

For some people, even after doing all of this, the numbers still don't add up. The repayments plus basic living costs come to more than what comes in. That's not a budgeting problem, it's a structural one, and there are solutions designed specifically for that situation.

The two main paths are:

A Part IX Debt Agreement is generally only an option if you owe more than $8,000 in unsecured debt and meet a few other criteria. If your debts are smaller than that, the steps in this article, combined with a hardship application and a chat with the National Debt Helpline, will almost always be enough.

If you'd like to understand whether any of the formal options might be relevant for your situation, you can speak to one of our specialists for free at Beyond Debt. There's no obligation, and we'll be straight with you about whether a formal solution makes sense or whether self-help is the better path.

The last thing worth saying is this: getting out of debt is roughly 5% knowledge and 95% behaviour. You now have the knowledge. The behaviour is the part nobody can do for you.

Two small things help more than people expect:

If your Instagram and TikTok feed is full of people showing off cars, holidays and luxury bags, your idea of "normal" is being skewed in real time. Unfollow accounts that make you feel behind. Replace them with #debtfree, #frugalliving, or accounts of Australians paying off debt openly. Your "reference group" matters more than you think.

On a piece of paper, list ten reasons you want to be debt-free. Less stress. A bigger emergency fund. A holiday with the kids. Being able to say yes to things. Move out. Whatever it is, keep that list in your wallet. Look at it on the days you want to give up. Becoming debt-free is one of the most genuinely life-changing things a person can do, and the small wins add up faster than you'd expect.

You don't need to be perfect. You just need to start. Most people who've done this say the same thing: they wish they'd started sooner.

We've put together a free 2026 budget planner spreadsheet built for the way Australians actually spend now: BNPL, subscriptions, food delivery and all. Click the button below to download it!

Beyond Debt is a trading name of DCS Group Aust Pty Ltd. Australian Credit Licence 382607. Registered Debt Agreement Administrator (RDAA #1126). The information in this article is general in nature and does not take into account your personal circumstances. Outcomes vary, and any formal insolvency option has consequences for your credit file and other parts of your life. For free, independent financial counselling, contact the National Debt Helpline on 1800 007 007.